Our collection of resources based on what we have learned on the ground

Resources

Q&A

What ad hoc checks should auditors in India do?

- June 2014

- Free Access

Auditors are required to check that any payment in cash or aggregate payments in cash totaling over INR 200,000 in one day are not claimed as a deduction (in accordance with Section 40A(3) of the Income Tax Act 1961), and also check other credit bala...

Q&A

Are there inventory auditing requirements for manufacturing companies in India?

- June 2014

- Members Access

Manufacturing businesses need to demonstrate that they have maintained their RG23 books and stock registers for manufacturing or processing materials. An auditor will verify that this has been done correctly, and will need to ascertain whether the RG...

Q&A

Are businesses required to give the auditor their management accounts opening ba...

- June 2014

- Free Access

Businesses are not required to give the auditor their management accounts opening balances, but should have them ready in the event that an auditor wants to check that the opening balances in those accounts have been carried forward correctly from th...

Q&A

Why should Indian company maintain a copy of their Permanent Account Number (PAN...

- June 2014

- Free Access

Companies must also ensure that they are properly maintaining photocopies of Permanent Account Number (PAN) cards for any contractors that come under tax deduction at source (TDS) applicability. If a company has not been provided with a contractor&rs...

Q&A

How can fraud be avoided in India?

- June 2014

- Free Access

Fraud can be avoided through the use of Audit and Attestation services. Most companies in India are required by law to have an Internal Audit department, which is given independence and which directly reports to the board of the company. Another way ...

Q&A

What is the difference between fraud and error in India?

- June 2014

- Members Access

The key difference between “fraud” and “error” often relates back to the intent to deceive, and distinguishing between the two can be challenging. Auditors are charged with exercising judgment when preparing their opinion for ...

Q&A

How can a company mitigate the risk of fraud in India?

- June 2014

- Free Access

Mitigating the risk of fraud begins with a robust governance structure that includes the audit of budgeting processes, ethics policies, quality control, monitoring procedures by senior management, and rotation procedures. Any weakness in an organizat...

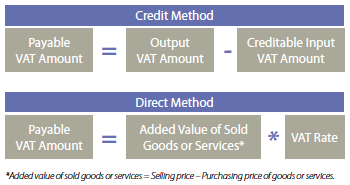

infographic

Two Methods for Calculating VAT in Vietnam

- June 2014

- Free Access

This infographic details the two methods for calculating value-added tax in Vietnam

Q&A

What does the Vietnamese Law on Amendment of Value-Added-Tax entail?

- June 2014

- Members Access

Vietnam’s main value-added tax (VAT) laws are based on The Law on VAT NO.13/2008/QH12 dated June 2, 2008 and Law No.31/2013/QH13 (the Law on Amendment of VAT) dated June 19, 2013. The Law on Amendment of VAT amends and adds to the Law on VAT by...

Q&A

Who can be subjected to value-added tax (VAT) in Vietnam?

- June 2014

- Free Access

Taxable persons in Vietnam are: Organizations and individuals producing or trading in VAT-liable goods and services in Vietnam, regardless of their business lines, forms and/or organizations; and Organizations and individuals importi...

Q&A

What are the value-added tax (VAT) rates for enterprises in Vietnam?

- June 2014

- Members Access

Vietnam has three VAT rates: zero percent, five percent and 10 percent. 10 percent is the standard rate applied to most goods and services, unless otherwise stipulated. Zero percent tax rate The zero percent tax rate applies to exported goods and se...

presentation

Cross Border Transactions Profit Repatriation and Funding of SMEs in China

- May 2014

- Members Access

Hannah Feng, Senior Manager of Corporate Accounting Services, analyses tax implications in five different case studies regarding cross border transactions and repatriation of profits.

Enquire for more information about our services, and how we can help solve challenges for your organization

Contact UsOur Clients

Discover our esteemed global clients across diverse sectors. We believe in providing our clients with exceptional service and a commitment to being their partner for growth in Asia.

See what our clients say about us